About Mantle Ridge

Who We Are

Mantle Ridge’s primary mission is to support the boards with which we engage, and to help them most effectively create durable long-term value for shareholders and other stakeholders.

Mantle Ridge’s structure is closely aligned with our “permanent ownership” mentality. None of our affiliated entities is a hedge fund or other investment vehicle with a structurally short-term incentive. This fundamentally differentiates us from other market actors who are known to engage with boards. Those who know us describe us as an engaged, long-term, owner-steward.

“The company is continuing to assure investors that it will deliver its promised rate of return. In the meantime, World Energy, which was initially guided to 2025 start, had a budget increase from $2.0 to $2.5 billion, experienced delays in receiving permits and is currently on hold. Louisiana Blue has had a budget increase from $4.5 billion to $7.0 billion, no off-take agreement, and is also delayed from the original guidance. NEOM initially did not have an off-take agreement, introduced commodity exposure and operational and technological risk, and significant capital commitments.”

“APD’s effort to return fire on Mantle Ridge’s track record by utilizing overtly dubious measurement dates and eschewing relevant industry benchmarks ultimately carves a fairly wide berth around credibility. We note Mantle Ridge has firmly addressed this issue with much more widely accepted analytical methodologies[.]”

“We believe the assortment of modestly reasoned metrics advanced by APD swiftly falters under withering critique from Mantle Ridge, which goes on to offer investors a substantially more comprehensive and transparent dissection of the Company’s operating performance and financial condition.”

“It is worth noting that tracking the progress of each project is not trivial for investors. Despite the company’s frequent appearances at investor conferences, direct questions are often met with vague answers, or assertions that the company cannot disclose information due to competitive reasons or confidentiality agreements with their partners. Cancellations and project delays are not proactively announced, as was the case with Yankuang, Indonesia, and World Energy, and certain unusual features of the structure are only disclosed after they begin affecting financials[.]”

The Mantle Ridge Approach

In ordinary course, Mantle Ridge works closely, collegially, and quietly with boards. Through iterative discussions that typically unfold over two to four months, we help boards restructure themselves. The reconstituted board typically compromises a contingent of ongoing directors (in each past case one more, or one less than a majority) plus a contingent of new independent directors. In each case, this process and the restructuring, have resulted in material outperformance vs. peers.

We do not take lightly the step of publicly nominating directors and soliciting their proxies. This has not been necessary since our founding in 2016. Because the Board shut down all engagement with our firm after five days, a solicitation has been necessary here.

Alignment with Long-Term Stakeholders

Our investment entities are a family of single-idea, special-purpose vehicles funded by long-term capital. A new set of entities is formed for each new investment, and each holds an exposure to just one company. They are of indefinite life, and enable the General Partner to maintain its equity interest indefinitely – well beyond when we may choose to return our partners’ capital. Upon the return of capital to our limited partners, the General Partner receives a performance allocation in the form of Company shares (i.e. there is no “cash out” or exit). These allocated shares, combined with those purchased outright by the General Partner, form the basis of the General Partner’s permanent equity interest and long-term alignment.

The power of our long-term alignment cannot be overstated. We remain committed to driving durable value improvement over the long term.

Setting the Record Straight:

Mantle Ridge Consistently Delivers Value Creation for Shareholders

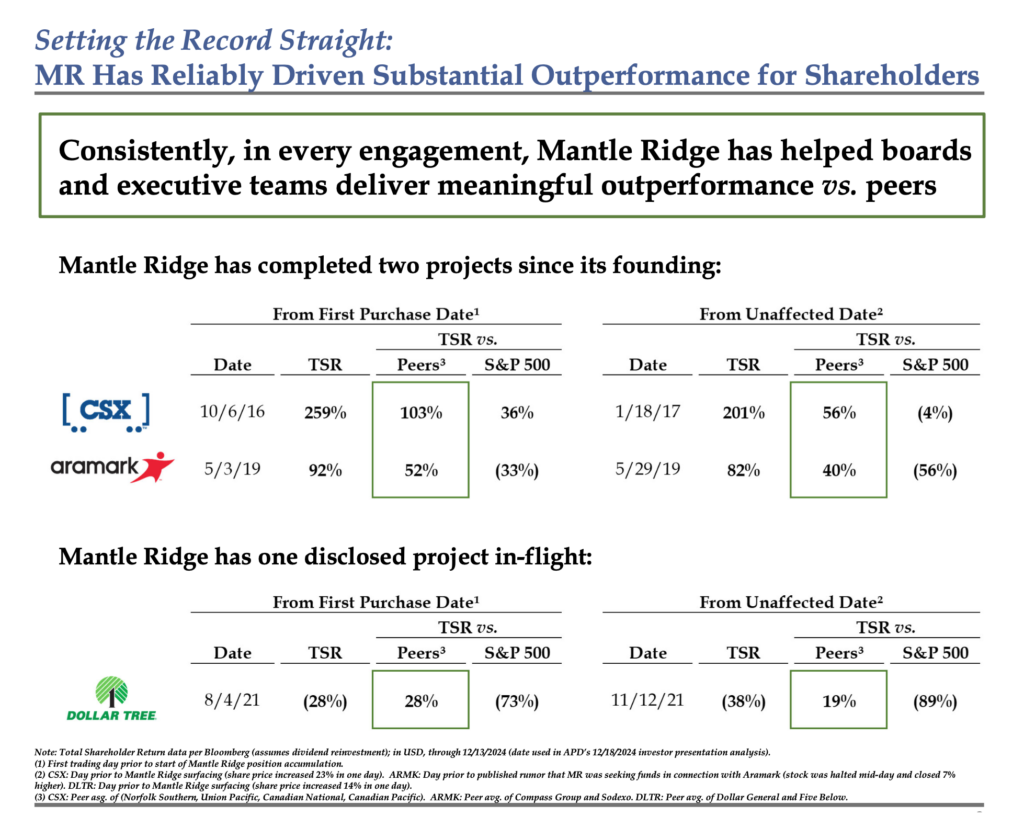

TSR Outperformance of 40% to 103% on Completed Projects

Each Mantle Ridge engagement has created value for shareholders, as measured by Total Shareholder Return (TSR) outperformance vs. relevant peers.

This is true when TSR is measured from any meaningful start date, including both (i) the date of Mantle Ridge’s first purchase of shares and (ii) the “unaffected date”1, i.e. the last trading day prior to public knowledge of Mantle Ridge’s involvement.

Depending on the chosen start date, Mantle Ridge has delivered TSR outperformance vs. peers ranging from 40% to 103% on completed projects. Inclusive of in-flight projects (e.g., Dollar Tree), and projects in which we played a leading role at a predecessor firm, the outperformance ranges from 19% to 345%.

- Outperformance relative to most relevant peers is the most meaningful measure of board and management performance, and shows the impact of Mantle Ridge’s involvement.

- Macroeconomic variables, regulatory changes, market dynamics, and other factors can impact industries very differently making performance comparisons across industries, and vs. diversified indices, difficult to interpret and potentially misleading.

APD presents Mantle Ridge’s record in a grossly misleading way:

- APD ignores the most relevant benchmark – performance vs. peers’

- APD’s chosen start date for the TSR calculations was after 41-60% appreciation following the start of Mantle Ridge’s accumulation of shares. Note that the upward share price pressure from Mantle Ridge’s purchasing 5%-19% of these companies, volume-driven speculation about activist involvement and our involvement, leaks, and other factors drive share price appreciation during our accumulation periods.

- APD’s chosen start date for the TSR calculations was after 30-35% appreciation following the date Mantle Ridge’s involvement was made public (i.e. since the “unaffected date”2), reflecting shareholders’ anticipation of change and value creation. By way of example, CSX, Dollar Tree, and Air Products’ shares appreciated 10-23% on the first trading day after our involvement was publicly confirmed.

Please review the supporting slides here to fully understand the truth about how Mantle Ridge creates value for shareholders.

APD’s misrepresentations of Mantle Ridge’s investment history is another example of why shareholder-driven change is urgent and necessary to get APD shareholders the truth, transparency, and performance they deserve.

The upcoming Annual Meeting offers APD shareholders our chance to begin a far better chapter. Mantle Ridge urges shareholders to vote the BLUE Proxy Card “FOR” Mantle Ridge’s Four Highly Qualified Director Nominees and “WITHHOLD” on the Company Nominees Charles Cogut, Lisa A. Davis, Seifollah “Seifi” Ghasemi and Edward L. Monser.

1 CSX: Day prior to Mantle Ridge surfacing (share price increased 23% in one day). ARMK: Day prior to published rumor that MR was seeking funds in connection with Aramark (stock was halted mid-day and closed 7% higher). DLTR: Day prior to Mantle Ridge surfacing (share price increased 14% in one day).

2 Id.